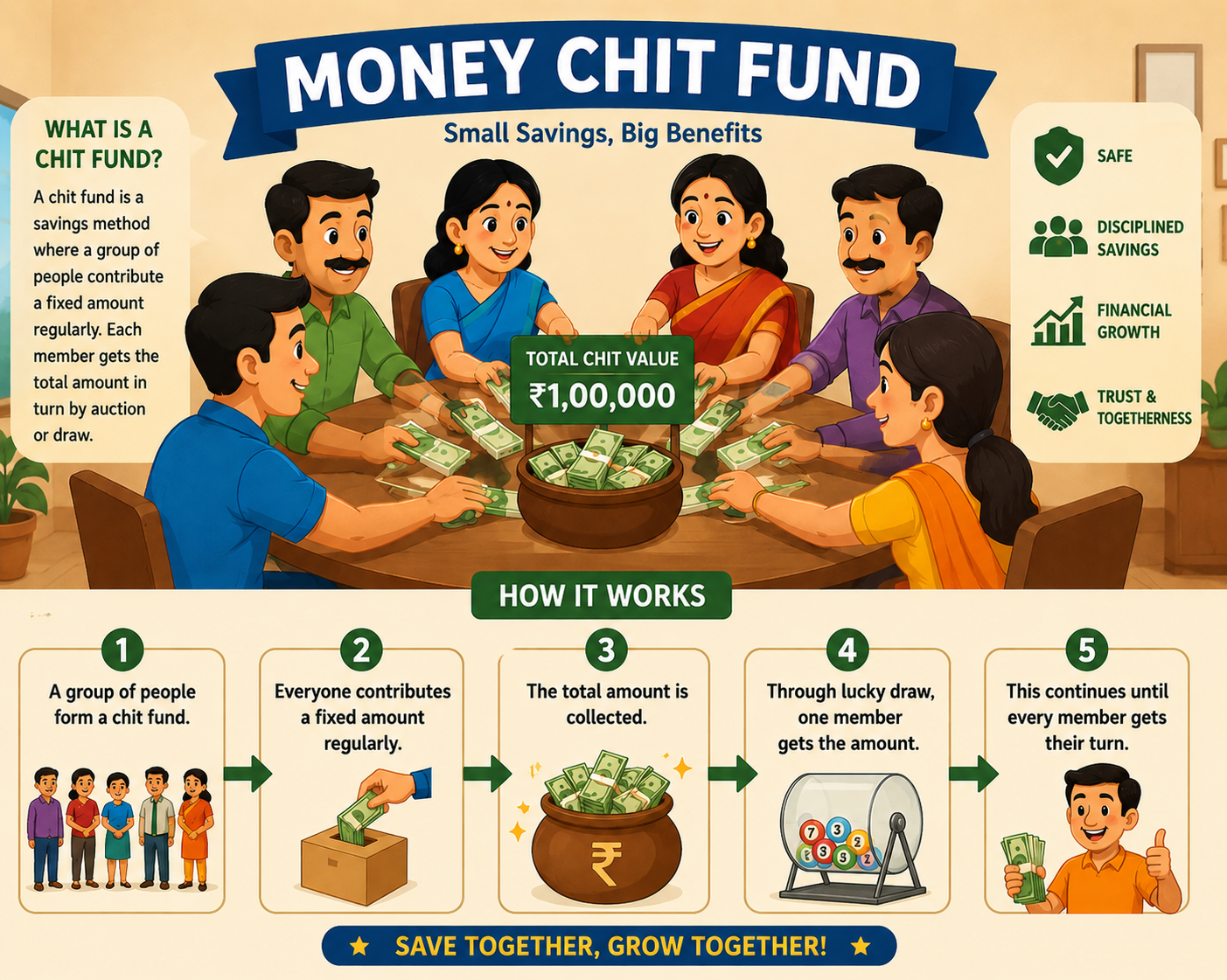

What is a Chit Fund?

A time-tested savings system where a group of people contribute, save, and borrow — all within a structured, transparent process.

How it works, in plain terms.

A chit fund is a rotating savings and credit system. A fixed group of members contributes a set amount each month into a common pool. Every month, one member gets to take the full pool amount through a lucky draw.

Think of it as a savings account and a loan facility rolled into one — but run by a community, not a bank. It's been a part of Indian financial culture for over a century.

The chit fund process.

Here's how a typical chit cycle works from start to finish.

Group Formation

A group of, say, 20 members is formed. Each agrees to contribute a fixed amount — let's say ₹5,000 — every month for 20 months.

Monthly Lucky Draw

Each month, an lucky draw is held. Members who need funds bid a discount. The member offering the highest discount wins the pool that month.

Prize Distribution

The winner receives the pool amount minus the discount. The discount is divided among all other members, reducing their monthly contribution.

Cycle Completes

This continues until every member has received the prize money once. Members who wait longer benefit from accumulated dividend savings.

Protected by law.

Chit funds in India are regulated under the Chit Funds Act, 1982, administered by the respective State Governments. Registered chit fund companies like Shree Aishwariyam Chits are audited, bonded, and required to maintain security deposits to protect subscribers.

Unlike unregistered schemes, a legal chit fund gives you complete transparency — you know exactly where your money is, and you have legal recourse if anything goes wrong.

Key safeguards

- Registered under the Chit Funds Act, 1982

- Regular government audits and inspections

- Mandatory security deposits by the foreman

- Transparent, witnessed auction process

- Legal documentation for every transaction

- Member dispute resolution framework